Welcome to the blog of inTAXicating.ca! Since 2008 we've been writing posts to help Canadians solve their tax issues with the Canada Revenue Agency. If you have any questions, or if you need assistance with any CRA matters including, but not limited to; Collections, Enforcement, Audits, Liens, Back-Filing, Assessments, Director's Liability, s160/325, Taxpayer Relief or the Voluntary Disclosure Program. If you have debt and are considering Bankruptcy or a Consumer Proposal, speak with us first. With over 10-years of CRA experience in the Collections division, our expertise is in the diagnosing and solving of the most complex tax problems.

Warren Orlans, the Director of inTAXicating Tax Services has completed his Profitable Giving Specialist accreditation which certifies that he is able to demonstrate understanding and proficiency in each of the following 4 areas;

The Tax Shelter Industry in Canada

The Regulations: Promoter Liability and Penalties, Third Party, and Civil Liability

Registered Profitable Gifting Arrangements and the Law

The Role of the Canada Revenue Agency in Regulating RPGAs

In addition to assisting Canadian Taxpayers who have fallen victim to Tax Shelter scams like the Global Learning and Gifting Initiative (GLGI), the Canadian Organization for International Philanthropy (COIP), the Relief Lending Group (RLG), Mission Life Financial Inc (MLF), Pharma Gifts International (PGI) and Integrated Receivables Management Inc / Integrated RM Inc (IRM).

inTAXicating provides Canada’s only full tax solution to assist Canadians solve all of their tax problems, including ones brought on by participating in tax shelters.

Below is only a snapshot of how to view a CRA debt related to a Tax Shelter / Gifting Arrangement and some of the options to start resolving the issue(s).

In order to reach a solution for Canadian Taxpayers the following things must be considered;

Ability to Pay according to you and,

Ability to Pay according to the CRA.

From there, you have only a few options;

Do nothing

Resolve the balance outstanding

Fight the CRA

Should you choose to resolve the balance outstanding, you again have only a few options;

Pay the balance in full

Ask the CRA for a payment arrangement, and prove you need one

Wait for the CRA to take it from you.

File a Consumer Proposal

File for Bankruptcy.

Keep in mind that the CRA does not “settle” debts like the IRS does. The only way to “settle” or pay less than the full amount of tax, penalties and interest, is through bankruptcy or a proposal.

While all of the Collections matters are in process, you are entitled to file for Taxpayer Relief and ask the CRA to return some or all of the penalties and / or interest which it has charged you. This application should be devoted time and effort to complete. It should never be a cookie-cutter application written by someone else because the CRA sees those and mass-denies them. Anyone trying to sell you a cookie-cutter application knows this and is “helping” you for the money and not because it’s the right thing to do.

Taxpayer Relief does not hold back Collections for doing what Collections does – trying to collect a balance owing – nor do CRA Collections care that a Taxpayer Relief application has been submitted.

A CRA review of a Taxpayer Relief Application can take upwards of a year. Be prepared for that delay and the interest that accumulates on your tax account should you wait to pay it later.

Having a trained set of eyes look over and edit a Taxpayer Relief application is a great idea because if you’re taking the time to submit an application, you want to make sure that you are putting your best work forward.

But ultimately, when looking at your options… All of your options, you want to make sure that your interests are being looked after first. You need an expert in CRA Collections, in Tax Shelters, and who can assist you with accounting, refinancing, insolvency and proposals and who can give you the best advice, the most cost effective advice and the advice that they would take if they were in your shoes.

inTAXicating Tax Services is that organization and we’re here to help you with all of that, and so much more. We associate ourselves with like-minded professionals who also understand that you are the client and that you need assistance and service.

If you have any questions about any tax shelter that you may have been involved in, and you need to know your specific options, contact us at info@intaxicating.ca

Are you Insolvent or do you just have Tax Troubles?

Don’t let the CRA decide this for you… They want you to do what is easiest for them! You need to do what is best for you!

In my experiences which included almost 11-years working in the Canada Revenue Agency (CRA), you should never allow the CRA to decide whether you can fix your tax problems or whether you should go bankrupt.

From the stand-point of a CRA Collections officer, going bankrupt is great because it removes the account from their inventory of accounts to collect / resolve.

Your file disappears from their inventory and re-appears in the CRA’s Insolvency Unit inventory.

From the perspective of the Collections Department, it’s case closed!

There are 3 ways a CRA Collections Office resolves one of their accounts;

1) Collect it / fix the compliance issue(s)

2) Write it off because they cannot collect it

3) Move the account to the Insolvency unit

Go Bankrupt!

The CRA’s Collections Officers are not allowed to tell you to go bankrupt. In fact, they are taught in their training that they are not allowed to do that, and that sentiment is reinforced at all future training they attend. As someone who trained CRA Collections staff for 5-years, I can confirm this fact.

Collections staff are not allowed to even suggest that you go bankrupt. They might confirm it, but that’s all they can do.

What CRA Collections can do, however, when they feel you are insolvent, is to force you into bankruptcy via their collection actions, which include but are not limited to;

Bank garnishment

Wage garnishment

Lien on a property

Enhanced garnishment to accounts receivables (in the case of a business)

All the while, why applying these garnishments, the CRA refuses to release the hold on the accounts.

They freeze every source of income that you might have and you are faced with the decision to come up with the funds to pay them, or file for a proposal or an assignment in bankruptcy.

In some cases, a bankruptcy is unavoidable and the right solution, but not in every case, which is why I strongly recommend speaking to someone who is looking after your interests first and foremost.

There are tax-related companies who are fronts for insolvency firms, so they might appear to want to help you, but they want you to file for bankruptcy, and there are other tax-service firms which gather your information and they unable or unwilling to help you, pass you along to a trustee.

You don’t want or need either of those.

You need a tax firm which has the experience in CRA’s collections, and who have the relationships with not only Insolvency firms, but mortgage brokers, reputable accountants and investment professionals so that you’re options are laid out for you to decide the best option.

Not the CRA.

In order to resolve your tax issues you need to disclose the details so your options can be determined, and you need your tax help to do the same.

Ask your tax-help the following questions;

Are you committed to finding me a tax-solution first.

If that solution is not going to be accepted by the CRA, what other options do you feel would work.

Don’t be weary if a firm wants to charge you a small fee to diagnose and plan out your solution.

You should be weary if they want to charge you a significant amount of money to diagnose it and not give you a plan. If they want to keep the plan a secret, and not educate you along the way, it’s because there is no plan.

Likely their solution it to drag you along the process knowing that the CRA will come along and lower the boom and then suggest to you that your only option is to conveniently have them file bankruptcy for you.

Don’t ask the CRA if you should go bankrupt. You might not like the answer.

If you owe money to the CRA and you’re not sure if the debt is a tax matter which can be resolved, or if bankruptcy or a proposal are better options, just ask! Send an email to info@intaxicating.ca and let’s talk! We’re here for you.

Insolvent or Tax Troubles? Don’t Let the CRA Decide!

In my experiences which includes almost 11-years working in the Canada Revenue Agency (CRA), you should never allow the CRA to decide whether you can fix your tax problems or whether you should go bankrupt.

From the stand-point of a CRA Collections officer, going bankrupt is great because it removes the account from their inventory of accounts to collect / resolve.

Your file disappears from their inventory and re-appears in the CRA’s Insolvency Unit inventory.

From the perspective of the Collections Department, it’s case closed!

There are 3 ways a CRA Collections Office resolves one of their accounts;

1) Collect it / fix the compliance issue(s)

2) Write it off because they cannot collect it

3) Move the account to the Insolvency unit

Go Bankrupt!

The CRA’s Collections Officers are not allowed to tell you to go bankrupt. In fact, they…

Just wanted to drop a quick note to all of you who called, emailed and hit me up on the blog or on social media that we’re back to work and trying to get to everyone as soon as possible.

If anyone has an urgent matter, please send an email to info@intaxicating.ca, in the subject line, please write “urgent” and that will be the top priority.

For new readers of this blog or who are seeing this blog through our website, here is what you need to know!

inTAXicating is a Canadian tax consulting business which provides solutions to Canadian Tax problems predominantly related to the Canada Revenue Agency (CRA), but not limited to the CRA.

With over 20-years experience in Canadian Tax (throw in some IRS tax, FATCA, Revenu Quebec, Cross-border matters and WSIB) combined with over 10-years working in the CRA in their collections division, you have the experience and expertise that no-one else can boast to have.

Our model is simple! Give you the truth based on the facts.

You get a free consultation and if it is determined that you can handle it best, or if your questions are quickly answered, then you are on your way.

If there are more complex matters which may eventually require greater expertise, then you have the option to handle you tax matters up to that point and then hand it over, or you may wish to hand it over right away…

It’s your taxes and you need to know what is being done and how to properly handle them going forward.

There are no magical cures for tax problems which took years and years to grow, so if anyone promises you a magic bullet, proceed with caution.

inTAXicating also believes that everyone who earns money needs to pay their taxes, however, they should pay what they owe, and in circumstances where there is no ability to pay, the government should understand that and give you a break.

No questions are bad questions.

I do not believe in the “natural person” being exempt from taxes because the CRA does not believe it, but I have spoken to many, many “de-taxers” and enjoy the conversations and helping them through the CRA’s prosecutions.

We specialize in all matters relating to CRA collections, specifically Directors Liability, Taxpayers Relief, s160 assessments, liens, and garnishments, RTP’s.

We provide audit representation, accounting (through a CA), as well as presenting the options to solve all tax matters including the ugliest and most complex tax matters. The messier the better!

In short, we want to help.

15 minute Consultation / responding to questions via email – free

Meeting – $250 plus HST (one hour meeting – detailed summary and recommended plan of action included)

Engagement – either hourly @ $250/hour or a fixed fee depending on the complexity and amount of work involved.

Accounting – best rates possible also related to the amount of work involved.

We try to stick to this model as best as humanly possible because it’s your money and you work hard for it, so you should not have to throw it away.

Every couple of days I receive a call from a taxpayer or corporation regarding huge sums of money they have paid to other so-called “tax solution” firms, without any apparent movement or resolution of their file. Usually these stories involve secrecy and the requirement for additional funds in order to bring the file to a close.

Would you go to a dentist who treated you like that?

Or have your vehicle repaired at a shop where you were not even sure they had any mechanics there?

When dealing with tax-related matters there should be no secrecy. There should be questioning whether work was done or not and there certainly should not be doubt that the job was not completed.

Unfortunately this happens more and more.

The representation you chose, when under fire by, not just by the CRA, but all areas of government, like the WSIB, RST, or CRTC, is far more important than you could possibly imagine. Especially in light of the fact that the CRA, for example, keeps a permanent diary record of your conversations and their attempts to resolve your tax file. They also carry forward an account summary every 6-months, so in the instance where an account has been transferred to another collector, that new collector will know within minutes how the CRA wants to treat you and / or your representative.

Lie to them.

Break promises.

Call them names, like the “taxman”.

It’s all there and its used against you… Forever.

Case in point:

A couple of years ago I met a couple of directors of a corporation who booked a 2-hour meeting with me for only $500 plus HST. They had come with the intention of having me assist them in negotiation with the Canada Revenue Agency (CRA) who were in the process of raising a Director’s Liability Assessment against them the unpaid debts of the Corporation they operated. They could not afford to pay the balance in full and were worried the CRA would take their house.

These directors had also heard about a way to reduce penalties and / or interest and they wanted more information.

They had already met with 2 other tax solution firms and one of them had fed the CRA with a sob story which the CRA did not buy, and after failing to return calls, and have any meaningful conversation with the CRA, disappeared with their money. The CRA kept trying to reach this representative and the directors had no idea how quickly the collections efforts had progressed and how upset the CRA had beceome.

The second firm charged them a lot of money, then set out to make a payment arrangement with the CRA, even accusing these directors of “fudging” their records in order to show less income than they actually had.

They were frustrated, had spent a lot of money and had now incurred the wrath of the CRA.

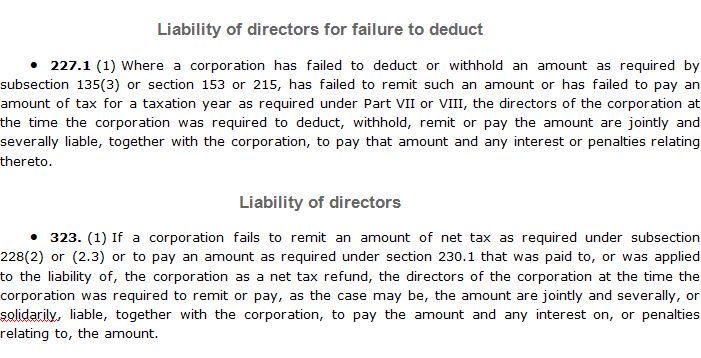

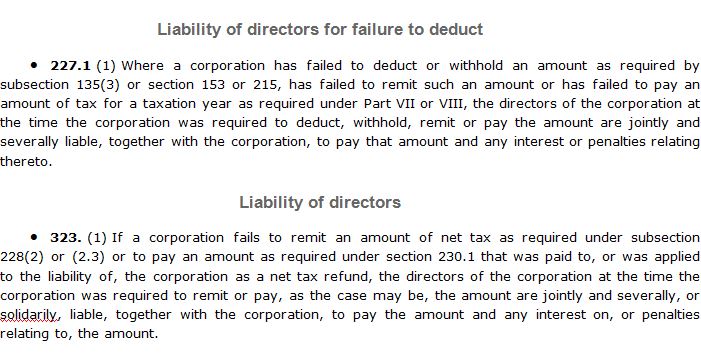

Then we sat down together to talk, and after only a few questions and a review of the notices they brought with them, I notified them of the statute of limitations the CRA must follow when raising a Director’s Liability Assessment under s.227.1 of the Income Tax Act and S323.1 of the Excise Tax Act, which was 2 years from the date the corporation ceased to operate or the date the director officially resigned from the corporation.

They said the business closed 3 years ago, and that their accountant had officially closed the corporation with the government.

We talked about the Taxpayer Relief Program and about key language to use when speaking to the CRA in order to begin to change the permanent diary record they keep on the corporation and the directors.

The meeting concluded.

I immediately pulled a corporate profile report, checked that against the date of the assessments the CRA were raising and found them to be beyond that limit.

I used the signed authorization forms to contact the CRA, and that 5-minute conversation resolved the account… Forever.

I provided the directors with a report of the meeting, including the information we discussed, the CRA’s actions to date, their likely next steps, plus recommendations about how to deal properly with the CRA going forward, and I explained to them that there was no need for a payment arrangement because the account had a zero balance.

Luck?

No.

Additional fees?

No.

Were they happy… You could say that. After they wiped away the tears and finished squeezing the life out of me, they talked about the relief they felt knowing this matter was finally behind them, and how they had other tax matters they wanted me to handle for them.

If representative #1 or representative #2 knew anything about collections or looked beyond their huge payout, they could have helped these directors with this assessment, with the 9-month-long audit that followed or the issues with WSIB, and the CRTC so that these directors owed nothing and their files were closed and in good order.

I had a nice long conversation with a client the other day regarding the potential that either the Canada Revenue Agency (CRA) or the Provincial government (in Ontario) were going to pursue a Director’s Liability assessment against him for the debts of his now-deceased corporation. Part of the discussion surrounded how the Canada Revenue Agency and the former Ontario Retail Sales Tax (RST) group handled assessments, and the criteria they used when reviewing whether or not to pierce the corporate shield, plus the importance of a due diligence defense.

Director’s Liability Section from the Income Tax Act and Excise Tax Act.

During my employment at the Canada Revenue Agency (CRA), I felt I needed to gain a more thorough understanding of Director’s Liability and figure out why there were so few assessments raised in our office compared to other offices. I personally had not raised any Director’s Liability assessments mainly because I was effective on the phone and combined with meetings, was able to resolve many debts prior to the assessment stage. Still, Senior Management encourage the Collections staff to utilize this collection tool more, so as the Resource and Complex Case Officer, I asked for, and was given, the Director’s Liability inventory to control.

By controlling the Director’s Liability inventory, that meant I needed to know the ins and outs of Director’s Liability – section 227.1 of the Income Tax Act and section 323 of the Excise Tax Act, because if anyone in our office wanted to raise an assessment, I would have to review their account, ensure all of the much-needed grunt work had been completed, then ensure they had spoken to the Director(s), given them sufficient notice, provided them time for a Due Diligence Defense, at which point I could sign off and begin to track the file.

After organizing that inventory and rolling out the new procedures, I began to scour the accounts in our office for potential Director’s Liability assessments, then, in addition to my other inventories, provide recommendations and suggestions to the staff on how to proceed if I felt there was a possibility for an assessment. Management decided instead of burdening the staff, I should just take those accounts I felt were ready for Director’s Liability assessments and work them, plus all of the other accounts I was tracking where assessments were raised too.

It was a fair amount of work, but more importantly, it was very enlightening, to review the government’s policies on Director’s Liabilities plus review the procedures in place, compare that to how other office’s handled their files and really tighten up the process. If an account was a sure-fire Director’s Liability assessment, it was raised, and if there was no chance, or not the right time, the file was returned to active collections.

I found the first common misconception around Director’s Liability was that the issuance of the Director’s Liability Pre-Assessment Proposal Letter (which notifies director’s that we are reviewing them for Director’s Liability) was being used as just another letter by the Collections staff to remind directors of their obligations, when in fact the CRA intended on using this letter to notify Directors’ that an assessment was beginning. Internally, the Canada Revenue Agency was actually starting to investigate the personal ability to pay of the director(s) at the time this letter was issued.

Going forward, that letter was not to be used lightly, and it was not to be sent to the Director(s) numerous times. A Director would then have the assessment raised against them and wonder why it was raised this time, and not earlier when one of those letters went out, so in order to prevent a possible loss in Tax Court, the decision was made to send it once, and then follow-up with the Due Diligence defense letter before raising the assessment.

Ignoring the Due Diligence defense letter (which happens often) meant the one opportunity a Director had to start their case on the record was lost, and with the CRA building their case in the permanent diary, the Director(s) stood little chance of preventing the Canada Revenue Agency from raising the Director’s Liability.

Once that waiting period passes, the file usually gets very quiet…

From the Director’s point of view, either the assessment is raised and they receive a letter from the CRA stating that, or the assessment is raised and the letter gets lost in the mail (tossed out), or the assessment is raised and before the Director is notified, their personal assets come under fire. There is of course, the possibility that nothing happens and the Director(s) are left in limbo, but without having a dialogue with the CRA, or experience around the policies and procedures, there is no way that the Director(s) will know when and if the CRA is coming – if at all.

Once raised, the Director(s) have quite limited options.

A recent court case, which I will highlight below demonstrates a situation where an assessment was raised, and in Tax Court, the decision was turned over and the assessment cancelled. I guarantee it won’t happen again, as the CRA will ensure their processes are tightened even more to close this loophole.

The case was Bekesinski V The Queen.

The link to the case on the website for the Tax Court of Canada, is here.

In this case, Bekesinski was the Director of a corporation who was personally assessed by the Minister of National Revenue (CRA) in the amount $477,546.08 for the corporation’s unremitted income tax (T2) and employer contributions of CPP and EI for payroll (source deductions) plus penalties and interest for the 2001, 2002 and 2003 fiscal years.

Under Director’s Liability, the CRA can assess directors for payroll and for GST/HST, but not Corporate Tax liabilities.

The Tax Court of Canada held that since the taxpayer had resigned as a director of the corporation more than two years after the CRA’s assessment, the CRA was statue barred from raising the Director’s Liability assessment.

This was something the CRA should have known before raising the assessment and something that the director (or his representatives) should have mentioned at any point during the pre-assessment proposal period, especially at the due diligence defense stage, but was never mentioned.

Brief Overview of the Facts

In 1992 the taxpayer purchased D.W. Stewart Cartage Ltd., a general cartage, trucking and warehousing company where he served as a Director of the corporation.

When the corporation fell behind on filing obligations and as the balance owing to the CRA began to grow, the Director began to receive numerous letters from the CRA warning him that he could be held personally liable for the corporation’s tax debts as a Director of the corporation. He did not notify the CRA at any time that he had resigned as a Director of the corporation.

On October 15, 2010 the CRA raised Director’s Liability and issued a Notice of Assessment (NOA) to the taxpayer for unremitted income tax, employer contributions plus penalties and interest in the amount of $477,546.08.

The Director then argued that he should not have been assessed as a Director because he resigned as Director of the corporation on July 20, 2006 by way of a Notice of Resignation which would have made the raising of the assessment statute barred.

The CRA argued that the taxpayer was in fact a director and that the taxpayer had backdated the resignation to qualify for the exception, which happens more than you could imagine, and to counter this trick, the CRA often requests an “ink date test” to determine the authenticity of the Notice of Resignation.

Unfortunately for the CRA, the results from the ink date test was excluded by the Tax Court because the CRA did not advise the Court that they felt the Notice of Resignation was back-dated. Even the judge felt the Notice of Resignation was backdated, however since the CRA failed to mention it, it was not open for review in the Court.

In summation, Bekesinski avoided Director’s Liability for the corporate tax debts due to a litigation misstep on the part of the CRA, a mistake they are unlikely to be repeat.

It is highly advisable for corporate directors to carefully document their resignations so as to avoid potential future Director’s Liability assessments, because I guarantee, the CRA will challenges to the authenticity of backdated resignations on each and every case going forward.

The elevator pitch, otherwise known as your ability to tell someone what you do for a living in 15-20 seconds without leaving out any critical details.

Wikipedia calls it this; “An elevator pitch, elevator speech, or elevator statement is a short summary used to quickly and simply define a person, profession, product, service, organization or event and its value proposition.”

The name “elevator pitch” reflects the idea that it should be possible to deliver the summary in the time span of an elevator ride of around 30 seconds.

The term originates from a scenario of an accidental meeting with someone important in the elevator where after the brief pitch, the other party is interested in learning more. thus continuing the conversation after the elevator ride or through en exchange of a business card or smart phone details.

As a tax consultant, I thought I had the perfect elevator pitch that went something like this; “I help people who have problems with the Canada Revenue Agency (CRA). I worked in the CRA for over 10-years – pretty much out of university – and worked my way up through the collections division until leaving for the private sector.”

I found it to be too long, and open for interruption so much that I would add details, such as that I completed 3-years of my accounting (CGA) designation and a 3-year MBA before leaving, or that I spent a significant part of my time at the CRA training the staff, handling the most complex accounts in the office and helping improve processes.

Then it became an elevator pitch for a 65-story building ride… To the top and all the way back down to the bottom.

Then I found an article in Forbes magazine which provided 6 alternatives to the elevator pitch so I tried them out to see if they worked better for me. The list is below:

1. The One-word pitch – for me, it is “TAX”. Then I watch their eyes gloss over.

2. The Question pitch – “Have you ever had (or have clients who had) problems with the Canada Revenue Agency (or Revenu Quebec, or the IRS, or WSIB, or the CRTC?)

3. The Rhyming pitch – Could not even try this.

4. The Subject line pitch – like sending an email to someone – mine would read something like “Former CRA collections officer helping people with CRA problems.”

5. The Story form pitch – I have thousands of stories… Literally. I usually break into one of these after my introduction.

6. The Twitter or 140 character or less pitch #WhatIAmAllAbout. I like this because it’s like using Twitter except that you really cannot tell someone that you “hashtag” Help People. But it does give you the opportunity to state your case in a brief number of words.

So practice your pitch – no matter which method you choose – and practice them out on people to see if it gets across the message you want it to. If not, maybe you would benefit from a different pitch or by adding or removing information to your existing pitch.

As for me… “I’m a former CRA officer who knows the CRA collections process, policy and procedures better than they do. I help people with a variety of tax issues including but not limited to negotiation, payment arrangements, liens, RTP’s assessments, and getting them current and out of debt. If there is a CRA issue, I have already seen it, and I know how to fix the problem.”

#x-taxer

Others make promises. I fix problems.

If the conversation continues I explain my services are for individuals, businesses, and professional organizations who cannot proceed further with a client due to their tax issues – ie/ getting a bank loan, renewing a mortgage, confirmation of actual amounts owing before filing for bankruptcy, wage garnishments on employees, or cleaning up past tax issues for separation agreements or divorce.

Most people are familiar with the concept of bankruptcy. Creditors are owed money, assets are liquidated and the liquidation proceeds are paid to creditors. The process is usually very difficult for the person filing bankruptcy as his/her assets may consist of a family home or a cottage, which possibly has been in the family for generations. The disruption can be devastating for the family and their children.

The Bankruptcy and Insolvency Act (BIA), the federal statute that governs bankruptcy and restructuring in Canada, provides an option other than bankruptcy.

The BIA allows an insolvent person whose aggregate debts are less than $250,000 (not including mortgages on residential property) to file what is known as a “consumer proposal”. A consumer proposal is not the same as bankruptcy, even though they are both governed by the same laws.

A consumer proposal is a formal settlement between a debtor and his/her creditors of all unsecured debts for an agreed upon amount. The settlement does not have to be for the full amount of all debts but can be for a fraction of the total owed. The debtor makes one monthly payment to the administrator of the proposal, who in turn makes dividend payments to the creditors.

More specifically, a person who is unable to meet their monthly debt payments meets with a qualified professional, who administers consumer proposals, and they discuss the ability of the debtor to make monthly payments. Together, they review the monthly income and expense statement of the debtor, as well as his/her net worth, to determine how much the debtor is able to pay each month. Once a monthly amount is determined the administrator notifies the creditors and helps to finalize a settlement agreement between the debtor and the creditors. Fifty percent (in dollar value) of the creditors must vote to accept the proposal for it to become binding on all.

The main difference between a consumer proposal and a bankruptcy is that in the case of the proposal the debtor’s assets are not liquidated. The debtor receives the same protection from creditors and collectors but retains control of his/her assets. The two obvious benefits are that there is no loss of assets and no family disruption.

One might ask “Well why don’t I just call all my creditors and work out my own settlement?” This will not necessarily work because, for example, if you have five creditors and you are able to settle with only

three of them, the remaining two are not forced to settle. They can still pursue you for the amounts they are owed. In a consumer proposal, all creditors are dealt with together and receive the same payment plan. As consumer proposals are governed by federal law, any settlement is enforced by the courts and creditors are required to accept the settlement in full and final satisfaction of all debts. So the debtor gets to keep his/her assets, he makes monthly payments to satisfy all debts over time and the creditors receive payments, which are greater than what they would have received if the debtor had filed bankruptcy.

Consumer proposals comprise an increasingly large percentage of overall personal insolvency filings in Canada. For records ending November 30, 2010, 31% of all consumer insolvencies in Canada were

consumer proposals. This is up dramatically from ten years ago when the majority filed for bankruptcy, having had no knowledge of the alternative.

In today’s economic environment, it’s important that people know what options they have to deal with debt. Canada’s insolvency laws mean that today, “Proposals are not just for marriage anymore”.

TODD HOWELL

Todd Howell is a licensed Trustee in bankruptcy and has over 13 years of experience in the bankruptcy and insolvency field. Todd is also a certified Insolvency Counsellor and a member of the Canadian

Association of Insolvency and Restructuring Professionals.

This article was originally published in Crowe Soberman’s quarterly business newsletter – Comments and is intended for clients of the firm. inTAXicating has been granted permission to repost this article solely for informative purposes. Should you require any assistance, we encourage you to contact the author(s) toll free at 1.877.929.2501, or in the GTA at 416.929.2500.

More articles can be found here; http://www.crowehorwath.net/SOBERMAN/services/advisory/Personal_Insolvency/Personal_Insolvency.aspx

I have always wanted to write a book to help Canadians deal with tax problems, or tax debts with the Canada Revenue Agency (CRA).

There is no better time than the present, so here is a preview;

Chapter 1.

Call me!

Chapter 2.

If you have a tax debt, tax problem, are behind on filing, made errors on your return, missed deductions or slips or if you owe money and cannot pay. You need a straight shooter who can tell you what to do and do so without costing you an arm and a leg.

Welcome to my company.

It is my goal to help each and every Canadian who has a tax problem through either a free 15-minute consultation, a one-hour meeting or through engaging my services.

I’m going to tell you what you need to know and not what you need to hear. If you are exposed to the CRA, I will tell you. If you are not legally required to pay a debt, I will tell you that too.

What I won’t do is mislead you into thinking that the CRA spends all day searching your keywords looking for you, unless you have done something criminally wrong, then I am recommending you speak with one of Canada’s top tax lawyers who will treat you in the same no-nonsense manner.

I also won’t lead you to believe that I have an army of former CRA staff at my disposal or that the CRA likes being referred to as the “taxman”. They do not. My network of CRA tax experts is vast and reside all over Canada. I have friends still working in the CRA and many who have left. I firmly believe that knowing what questions to ask is much more valuable than the answers given. I know what questions to ask, and I will ask them for you.

I do, however, have 10-years of experience at the Canada Revenue Agency – as a collector – and as a resource officer, field officer, team leader, and I have significant experience in fairness / taxpayer relief, managing the Director’s Liability and s.160 inventory, and for 5-years, I trained the collections staff at Canada’s largest Tax Services Office how to do their jobs. I cannot and will not list all the areas of the CRA that I worked in, because I wanted to learn, experience and help taxpayers while working there and I still want to do the same now that I am on the other side of the negotiating table.

Common sense tells me that if you have a tax, collections, or enforcement problem, you do not need a trustee, or a tax lawyer, or an accountant, but you need a former CRA collections expert to steer you clear of trouble.

Don’t let the CRA or other “tax” firms decide that you need to go bankrupt. You decide!

If you need forms filed with the CRA, or tax returns prepared for individuals or businesses, I work with the best accountants and accounting firms who share my philosophy of putting you first. Together we make sure your past filings are accurate and that you have claimed the correct amounts legally allowed. We don’t add things or make up deductions because that is what gets you in trouble.

My firm is Toronto-based, however accessible throughout Canada and around the world – as my clients have found out.

I’m not going to pull out a horse and pony show and try to entice you with fancy expensive ads which I will need to charge you extra to pay for – but I’m going to listen, process, and advise you what to do based on my experiences and based on 17-years of handling matters with the CRA, IRS, Revenu Quebec and with WSIB and the CRTC. I spent the majority of my time at the CRA working on the corporate side, so GST/HST, payroll, corporate tax and personal taxes are all in my areas of expertise.

I will tell you what the CRA is doing, and what they will be doing next. It’s nice to be a step ahead!

And throughout this whole process, you have to understand that the CRA will be working with us to resolve your tax matter and not working against us. It’s what they get paid to do. The only difference is they do it with us and not against us.

Conclusion:

So, why reach out to me? Why not!

I can be reached at info@intaxicating.ca, or by phone at 416.833.1581.

Pretty much everyone wants it at some point in their life.

Most of the people who have it do not know how to use it properly.

To be honest, few will ever get it.

The most important thing to know about power is that it is most successful when used in two ways; either by declaring yourself King and having your cronies keep everyone else at bay by whatever means possible, or secondly by taking the time to get key players on your side and using your network to help you maintain power but all along helping those around you learn and grow, and they help everyone else under them do the same.

Which model do you think is most often associated with government tax collections agencies?

Having spent a lot of time working at the Canada Revenue Agency (CRA) in the collections and enforcement division and being responsible for training collections, enforcement and audit staff there I can honestly say not as many staff there who feel you have to do what they say no matter the consequences as you would think.

It is true that there are employees of the CRA who feel that being in a position of power allows them to do things, say things and act in a manner which is improper or unjustified. There are also staff there who take their positions of power to a whole new level and they let their egos control their decision-making process which means they wield power in order to realize an outcome in their best interest, not yours.

I have seen how power corrupts and the result is never easy to correct.

The CRA has a lot of power.

Throughout my decade of employment at the Canada Revenue Agency I was surprised with how much power the Agency has and how many taxpayers feared this power. I could hear collection officers tell taxpayers that they could clean out their bank accounts like “this!” (Insert snapping of fingers sound here), which is true, but also not true. I learned to be subtle in my use of my apparent super-powers and the way I used my power was to visit my clients and by always making sure that when sitting with a taxpayer / representative that my chair was at its highest so that I would be looking down at them. It was all I needed when dealing with the career tax evaders because it worked, but it was a tactic not necessary when dealing with 99% of the people I met with.

However, we already know that the CRA has a lot of power and in most cases before they use it, they are going to let you know first by phone, letter or a visit to your home or place of employment. Once the CRA has decided they need to use their powers they are bound by the guidelines set out in the Income Tax Act and Excise Tax Act and by policies and procedures set out in their tax office. The extent to which they use their powers is either their decision or it is influenced by their team leader or manager.

Once the CRA starts using their powers, your ability to control the outcome diminishes greatly. What you can control, is how much power you will ALLOW the CRA to use against you.

This is done by being proactive – reading notices, asking questions and keeping all your paperwork in one spot where you can access it once it is asked for. But if you are past that point, or if it is just not possible, then you can take power back by enlisting the help of people who know the CRA policies, procedures and most importantly, their techniques and tactics.

If the CRA knew they were dealing with someone who knew more about their job, more about their techniques and more about how quickly they need to take an action which they claim is urgent, then the playing field is changed forever.

Having someone there to look after your best interests, who will tell you what the best plan of action for you, and you only, then taking that plan to the CRA and telling them the same is the best way to always level the playing field. Negotiating is always easier when you know more than your opponent.

So please, if you have a tax problem, old or new, and you have been spinning your wheels with the CRA, the IRS, the MRQ, WSIB or the CRTC, don’t let it continue any longer. Come visit inTAXicating.ca, or send us an email at info@intaxicating.ca and take advantage of our free consultation to leave how to put these issues behind you once and for all.

Have you ever been put in a position where you accepted something which was not in your best interests because the other side had all the power?

Canada Revenue Agency (Photo credit: John Bristowe)

Working in the Canada Revenue Agency for almost 11-years, I learned a thing or two about how the CRA operates as well as what is a red flag for them and what the CRA often let’s slide. It helps when I negotiate with them that I know their policies, procedures and how to navigate their systems as well as they do, or even better. I’ve used this knowledge to help my clients save millions of dollars of taxes.

With that in mind, I want to help you save unnecessary expenses, so I decided to reveal the 8 Biggest Taxation No-No’s EVER.

8. Try and do it yourself. Taxation is a complicated topic for many and if you don’t live and breathe tax then you should consider either hiring someone to help you along or at the very least hire someone to set you up correctly and who will take the time to learn about you and your business so that you are getting all of the tax deductions and credits available to you all the time.

7. Think that you are above taxation. Everyone pays taxes no matter their income level; whether it be income tax, payroll tax, or consumption tax. To think that there is a magic “Pay no tax” card is a huge mistake and the CRA does not take “detaxers” or the underground economy lightly..

6. Brag about not paying taxes / scamming the government. Our tax system here in Canada is a self-assessing system with the government’s responsibility being the checks and balances. It’s not that they don’t trust you but… They don’t trust you, which is why they have huge departments responsible for catching the tax cheats. If the government doesn’t get you, your ego might;

5. Post information online about yourself or your business and think that the government will not see it and use it against you. The “government” are a bunch of people like you and I who are trying to make a living. If you claim you are suffering from financial hardship yet post pictures on Facebook showing yourself living it up, or if you claim to be Canadian and your profile states that you are born in the US, the collectors or auditors will find it and us it against you.

4. File late, miss installment payments or fail to make remittances. All this will do is add penalties and interest onto your tax account and there are very few excuses the government will accept to have them reversed or cancelled. Many large tax debts start in just this way.

3. Carry a balance. If at all possible it is critical to make sure that you do not carry a balance with the CRA. With interest being charged at a floating rate of just over 10%, compounding daily, your balance can grow at a shocking rate. The CRA is not a bank and you should not think it’s okay to treat their debt as a bank loan.

2. Don’t be afraid to search online for your tax advice. Not only has the CRA moved to strengthen their online presence but there are a lot of professionals online who have posted their experiences with the CRA and steps they took to resolve tax problems for themselves and their clients. Anyone suggestion otherwise is doing so to avoid you from finding out there are other – better – tax solution providers in Canada.

1. Thinking that anyone can help you. This is the absolute biggest tax no-no I have encountered in 17-years of taxation. If you have an electrical problem at home, do you call a plumber? Would you ask a dentist to perform open-heart surgery? How about asking a former auditor to help you with a collections problem, or an appeals officer to help you correct your payroll nanny account issues? How about going to an Insolvency firm to have a lien removed from you house which was placed there by CRA collections?

It doesn’t make sense but don’t get me wrong. If you have created a tax crime, such as tax evasion, you will need a tax lawyer, and if you need tax returns prepared, they need to be done by an accountant, and a former CRA auditor is the right solution if you have a difficult, complex corporate tax audit underway,

In taxation it is critical that you have experience on your side when you work to resolve your tax issues and understanding the way the CRA operates is more important than you could imagine.

Tax debts begin with audit or compliance issues.

Then they go to collections.

Collections leads to enforcement – garnishments, requirements to pay (RTP), liens, seizures, director’s liability, and much more.

You need experienced former collections staff to help you, and with almost 11-years of progressive collections experience in all areas, from collector to resource officer, to team leader, believe me when I say that experience helps!

When your representative knows more than the collector, or trained that collector, you know you have the best representation possible.

To leave your $250,000 tax liability to anyone else would keep me up at night too.